Why Alberta Mortgages Need a Different Plan

Alberta doesn’t just offer better rates—it offers a whole different way to play the real estate game.

Whether you're leaving BC or Ontario, buying your first home, or planning to build wealth through multiple properties, the question isn't just fixed vs. variable. It's: What's the right mortgage strategy for everything you're trying to do?

In 2025, that question matters more than ever.

Rates Are Easing—But That’s Just the Surface

The Bank of Canada’s overnight rate is currently 2.75%, with the prime rate at 4.95%. Variable mortgages, usually priced around Prime – 0.90%, could land near 3.55% if rate cuts happen later this year. Fixed rates for insured 5-year terms are forecasted between 3.82% and 4.00%.

These are great rates—especially compared to where we’ve been. But they only tell a fraction of the story. Because here in Alberta, lower rates mean more opportunity, not just smaller payments.

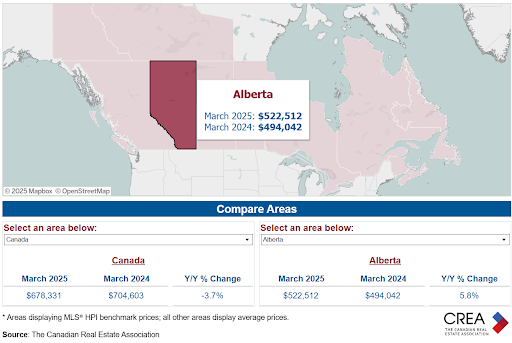

Why Alberta Buyers Are in a Different Position

Alberta continues to outpace the rest of Canada in almost every meaningful way. The average home price here is hundreds of thousands less than in BC or Ontario. Interprovincial migration is strong. Jobs are up. Taxes are low. And investors are seeing some of the best rental yields in the country.

The Province’s 2024–2025 economic outlook predicts 2.9% GDP growth, thanks to job creation, population growth, and ongoing housing demand. This isn’t just a good market—it’s a growing one.

“Alberta’s real GDP is expected to grow by 2.9% in 2025, outpacing national projections.”

(Source: Province of Alberta Economic Outlook, March 2024)

Families we work with aren’t just making a move—they’re making a lifestyle shift. Some sell in Ontario or BC and buy two homes here: one to live in, one to rent. Others relocate for opportunity, build new, or help their adult kids get into the market sooner. These aren’t basic mortgage clients. These are people leveraging Alberta.

Strategy First. Rate Second.

When you work with Merge, we start with a real conversation. Are you buying now or later? Do you plan to hold one property or pick up more? Will you refinance in a year or two when rates drop? Are you helping family or investing in the future?

We map it all out. Then—and only then—do we talk about fixed vs. variable, or whether a HELOC or alternative solution makes sense. Because at the end of the day, rate isn’t the product—strategy is.

Fixed or Variable? Here’s How We Break It Down

Fixed rates are best when stability matters. If you’re settling into Alberta, managing a strict budget, or sharing ownership with family, knowing your exact monthly payment can give you peace of mind.

Variable rates might make more sense if you're flexible, planning to refinance, or want the option to break your mortgage early with smaller penalties. And if you believe—like many economists do—that rates will trend down into 2026, it could mean meaningful long-term savings.

CREA hasn’t released April housing data yet, but they expect demand to rebound as rates fall. In Alberta, that rebound is likely to be steady—not frenzied—giving serious buyers and investors room to move.

“Sales are expected to pick up through the back half of the year... price growth will likely remain modest.”

(Source: CREA Housing Forecast, April 2025)

Why Merge? Because We Think Bigger—Just Like You

If you’re moving to Alberta for more space, better investment value, or a long-term plan for your family—we’re already aligned.

We work with buyers across Alberta, BC, and Ontario. We specialize in transition plans, multi-property strategies, and helping you use Alberta’s advantages to reshape what homeownership or investing can look like.

📞 587.370.4311

📧 jarrod@mergemortgage.ca

Sources: